Understanding how economies work helps us make better decisions about... Show more

Sign up to see the contentIt's free!

Access to all documents

Improve your grades

Join milions of students

Knowunity AI

Subjects

Triangle Congruence and Similarity Theorems

Triangle Properties and Classification

Linear Equations and Graphs

Geometric Angle Relationships

Trigonometric Functions and Identities

Equation Solving Techniques

Circle Geometry Fundamentals

Division Operations and Methods

Basic Differentiation Rules

Exponent and Logarithm Properties

Show all topics

Human Organ Systems

Reproductive Cell Cycles

Biological Sciences Subdisciplines

Cellular Energy Metabolism

Autotrophic Energy Processes

Inheritance Patterns and Principles

Biomolecular Structure and Organization

Cell Cycle and Division Mechanics

Cellular Organization and Development

Biological Structural Organization

Show all topics

Chemical Sciences and Applications

Atomic Structure and Composition

Molecular Electron Structure Representation

Atomic Electron Behavior

Matter Properties and Water

Mole Concept and Calculations

Gas Laws and Behavior

Periodic Table Organization

Chemical Thermodynamics Fundamentals

Chemical Bond Types and Properties

Show all topics

European Renaissance and Enlightenment

European Cultural Movements 800-1920

American Revolution Era 1763-1797

American Civil War 1861-1865

Global Imperial Systems

Mongol and Chinese Dynasties

U.S. Presidents and World Leaders

Historical Sources and Documentation

World Wars Era and Impact

World Religious Systems

Show all topics

Classic and Contemporary Novels

Literary Character Analysis

Rhetorical Theory and Practice

Classic Literary Narratives

Reading Analysis and Interpretation

Narrative Structure and Techniques

English Language Components

Influential English-Language Authors

Basic Sentence Structure

Narrative Voice and Perspective

Show all topics

144

•

Updated Mar 12, 2026

•

Pasindi Lahandapurage

@pasindilahandapurage_kqvo

Understanding how economies work helps us make better decisions about... Show more

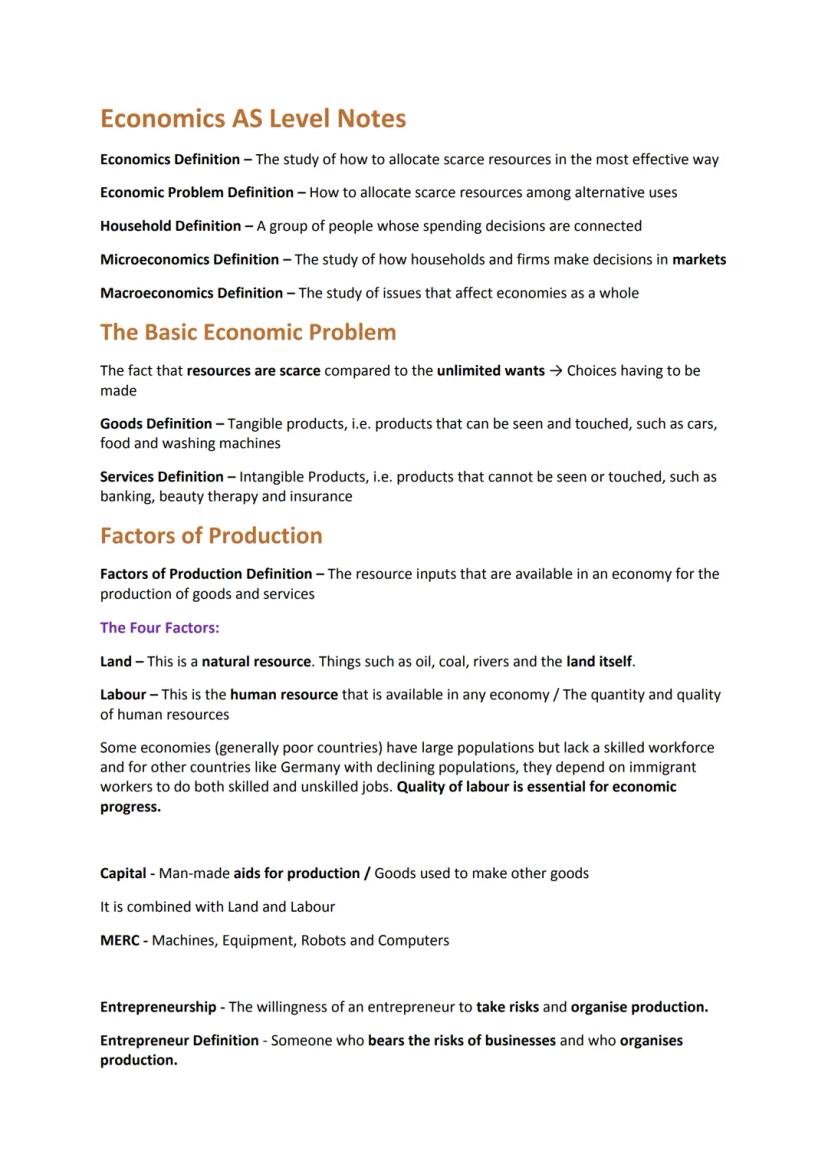

The foundation of economics centers on managing scarce resources effectively in a world of unlimited wants. When studying Economics AS level notes on factors of production, it's crucial to understand how resources are allocated among competing uses.

The four fundamental factors of production form the backbone of economic activity. Land encompasses all natural resources like oil, minerals, and agricultural land. Labor represents the human workforce, including both skilled and unskilled workers. Capital consists of man-made tools and equipment used in production . Entrepreneurship provides the crucial element of risk-taking and organizational capability needed to combine these factors effectively.

Definition: Factors of Production are the resource inputs available in an economy for producing goods and services. These include land, labor, capital, and entrepreneurship.

Understanding how households make economic decisions is vital for grasping both microeconomics and macroeconomics household decisions. Households must constantly make choices about consumption, saving, and resource allocation, all while facing the constraint of scarcity.

The economic problem of scarcity necessitates making choices about how to use limited resources. Every economic decision involves an opportunity cost - the next best alternative that must be foregone. This fundamental concept shapes how individuals, businesses, and nations make decisions.

Highlight: Factor endowments - the stock of factors of production available to an economy - significantly influence a country's economic potential and development path.

Production involves transforming inputs into outputs of goods (tangible products) and services (intangible products). The quality and quantity of factor endowments largely determine a country's productive capacity and economic prosperity.

Understanding these relationships helps explain why some nations prosper while others struggle. Countries with abundant and high-quality factor endowments generally have greater productive potential and economic opportunities.

International specialisation advantages and disadvantages play a crucial role in global economic development. When countries specialize in producing goods and services where they have a comparative advantage, it leads to increased efficiency and output.

Example: A country with abundant fertile land might specialize in agricultural products, while another with highly skilled labor might focus on technological products.

However, specialization carries risks. Weather-dependent industries can face severe disruptions from natural disasters. Over-specialization can lead to de-industrialization in some sectors. Additionally, changing consumer preferences or depleting resources can create economic hardships for specialized economies.

The key to successful international specialization lies in balancing the benefits of increased productivity and expanded trade opportunities against the risks of over-dependence on specific sectors or resources.

The Production Possibility Curve (PPC) illustrates the maximum output combinations an economy can achieve with its current resources and technology. This concept helps understand productive efficiency, allocative efficiency, and economic growth.

Vocabulary: Productive efficiency occurs at any point on the PPC, while allocative efficiency involves choosing the optimal combination of goods to produce.

Economic growth, represented by an outward shift of the PPC, can occur through various means. Quantitative growth happens when there's an increase in resource availability, such as through population growth or capital accumulation. Qualitative growth occurs through technological advancement and improved resource quality, such as better education and training.

Understanding these concepts helps explain how economies can expand their productive capacity and achieve sustainable growth over time.

Natural disasters significantly impact a nation's production capabilities, which can be clearly illustrated through Production Possibility Curves (PPC). When examining how events like earthquakes and tsunamis affect production, we see a distinct leftward shift in the PPC, indicating reduced production capacity across all sectors.

The relationship between different sectors, such as manufacturing and agriculture, demonstrates how natural disasters create widespread economic disruption. When resources become constrained due to catastrophic events, the economy's ability to produce different combinations of goods diminishes uniformly, resulting in the entire PPC shifting inward.

Definition: A Production Possibility Curve (PPC) represents the maximum possible production combinations of two goods that an economy can achieve with its available resources.

Understanding imperfect substitutes is crucial when analyzing PPC shifts. The curved nature of the PPC, rather than a straight line, indicates that resources cannot be perfectly substituted between different production processes. This reflects real-world limitations in resource allocation and production flexibility.

Economic systems serve as the fundamental framework determining how societies allocate their resources. In Microeconomics and macroeconomics household decisions play a crucial role in shaping these systems, whether in market economies, command economies, or mixed economic systems.

Market economies operate through the price system, where supply and demand forces determine resource allocation. Command economies, conversely, rely on central planning and state ownership. Mixed economies combine elements of both systems, allowing for both market forces and government intervention.

Highlight: The price system in market economies serves as an automatic mechanism for resource allocation, while command economies rely on centralized planning decisions.

These different economic systems each present unique advantages and challenges in addressing the fundamental economic questions of what to produce, how to produce it, and for whom to produce. The effectiveness of each system depends on various factors including social goals, resource availability, and technological capabilities.

Free market economies excel in promoting innovation and efficiency through competition. They provide consumer choice and typically generate higher economic growth rates compared to command economies. However, they may struggle with providing public goods and addressing income inequality.

Command economies, while often criticized for inefficiency, can better ensure the provision of public goods and maintain more equitable income distribution. They can also implement environmental protection measures more directly, though often at the cost of reduced economic dynamism.

Example: In a free market economy, private companies might underinvest in public transportation infrastructure, while a command economy can directly allocate resources to such projects regardless of immediate profitability.

The debate between these systems highlights the fundamental tradeoffs between efficiency and equity, innovation and stability, individual freedom and collective planning. Understanding these tradeoffs is crucial for evaluating economic policy decisions and their societal impacts.

International specialisation advantages and disadvantages significantly impact both firms and workers in the modern global economy. Specialization increases productivity and efficiency through focused expertise development and the use of specialized machinery.

For firms, specialization enables increased output, improved quality, and potential economies of scale. Workers benefit from higher wages in specialized roles and enhanced skill development in their specific areas. However, both parties face certain risks and limitations.

Vocabulary: Division of Labor refers to the breakdown of production processes into specialized tasks, enabling increased efficiency but potentially leading to worker monotony.

The disadvantages include reduced flexibility for firms and potential worker boredom from repetitive tasks. Firms may face higher training costs and dependence on specific suppliers, while workers risk skill degradation in other areas and possible technological replacement. Understanding these tradeoffs is essential for businesses making organizational decisions and workers planning their career development.

Consumer and producer surplus are fundamental concepts in Economics AS level notes on factors of production that help us understand market efficiency and welfare. These concepts illustrate how both buyers and sellers benefit from market transactions.

Consumer surplus represents the economic benefit buyers receive when they purchase a product for less than what they were willing to pay. When market prices decrease, consumer surplus increases, creating greater economic value for buyers. This relationship demonstrates how price changes directly impact consumer welfare and purchasing decisions in Microeconomics and macroeconomics household decisions.

Producer surplus occurs when sellers receive more for their products than the minimum amount they would have accepted. This concept is crucial for understanding market dynamics and how prices affect business profitability. When analyzing producer surplus, we must consider supply curve elasticity and market price fluctuations to determine the total economic benefit producers receive.

Definition: Consumer surplus is the difference between what consumers are willing to pay and what they actually pay, while producer surplus is the difference between what producers receive and their minimum acceptable price.

Example: If a consumer is willing to pay $10 for a book but only pays $7, their consumer surplus is $3. Similarly, if a producer would accept $5 for the book but sells it for $7, their producer surplus is $2.

Price changes significantly impact both consumer and producer surplus, demonstrating key principles of International specialisation advantages and disadvantages. When prices decrease, consumer surplus typically increases as buyers can purchase goods for less than their maximum willingness to pay. This creates additional economic value and increases overall market efficiency.

The magnitude of changes in consumer and producer surplus depends on several factors, including the elasticity of demand and supply curves. Steeper curves result in larger surplus changes when prices shift, while flatter curves lead to smaller changes. This relationship helps economists analyze market outcomes and predict the distribution of economic benefits.

Understanding these surplus concepts is essential for analyzing market efficiency and policy impacts. When evaluating market interventions or price controls, economists consider how changes affect both consumer and producer surplus to determine overall economic welfare effects.

Highlight: The size of surplus changes depends on:

Our AI companion is specifically built for the needs of students. Based on the millions of content pieces we have on the platform we can provide truly meaningful and relevant answers to students. But its not only about answers, the companion is even more about guiding students through their daily learning challenges, with personalised study plans, quizzes or content pieces in the chat and 100% personalisation based on the students skills and developments.

You can download the app in the Google Play Store and in the Apple App Store.

That's right! Enjoy free access to study content, connect with fellow students, and get instant help – all at your fingertips.

App Store

Google Play

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan S

iOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha Klich

Android user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

Anna

iOS user

I think it’s very much worth it and you’ll end up using it a lot once you get the hang of it and even after looking at others notes you can still ask your Artificial intelligence buddy the question and ask to simplify it if you still don’t get it!!! In the end I think it’s worth it 😊👍 ⚠️Also DID I MENTION ITS FREEE YOU DON’T HAVE TO PAY FOR ANYTHING AND STILL GET YOUR GRADES IN PERFECTLY❗️❗️⚠️

Thomas R

iOS user

Knowunity is the BEST app I’ve used in a minute. This is not an ai review or anything this is genuinely coming from a 7th grade student (I know 2011 im young) but dude this app is a 10/10 i have maintained a 3.8 gpa and have plenty of time for gaming. I love it and my mom is just happy I got good grades

Brad T

Android user

Not only did it help me find the answer but it also showed me alternative ways to solve it. I was horrible in math and science but now I have an a in both subjects. Thanks for the help🤍🤍

David K

iOS user

The app's just great! All I have to do is enter the topic in the search bar and I get the response real fast. I don't have to watch 10 YouTube videos to understand something, so I'm saving my time. Highly recommended!

Sudenaz Ocak

Android user

In school I was really bad at maths but thanks to the app, I am doing better now. I am so grateful that you made the app.

Greenlight Bonnie

Android user

I found this app a couple years ago and it has only gotten better since then. I really love it because it can help with written questions and photo questions. Also, it can find study guides that other people have made as well as flashcard sets and practice tests. The free version is also amazing for students who might not be able to afford it. Would 100% recommend

Aubrey

iOS user

Best app if you're in Highschool or Junior high. I have been using this app for 2 school years and it's the best, it's good if you don't have anyone to help you with school work.😋🩷🎀

Marco B

iOS user

THE QUIZES AND FLASHCARDS ARE SO USEFUL AND I LOVE Knowunity AI. IT ALSO IS LITREALLY LIKE CHATGPT BUT SMARTER!! HELPED ME WITH MY MASCARA PROBLEMS TOO!! AS WELL AS MY REAL SUBJECTS ! DUHHH 😍😁😲🤑💗✨🎀😮

Elisha

iOS user

This app is phenomenal down to the correct info and the various topics you can study! I greatly recommend it for people who struggle with procrastination and those who need homework help. It has been perfectly accurate for world 1 history as far as I’ve seen! Geometry too!

Paul T

iOS user

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan S

iOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha Klich

Android user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

Anna

iOS user

I think it’s very much worth it and you’ll end up using it a lot once you get the hang of it and even after looking at others notes you can still ask your Artificial intelligence buddy the question and ask to simplify it if you still don’t get it!!! In the end I think it’s worth it 😊👍 ⚠️Also DID I MENTION ITS FREEE YOU DON’T HAVE TO PAY FOR ANYTHING AND STILL GET YOUR GRADES IN PERFECTLY❗️❗️⚠️

Thomas R

iOS user

Knowunity is the BEST app I’ve used in a minute. This is not an ai review or anything this is genuinely coming from a 7th grade student (I know 2011 im young) but dude this app is a 10/10 i have maintained a 3.8 gpa and have plenty of time for gaming. I love it and my mom is just happy I got good grades

Brad T

Android user

Not only did it help me find the answer but it also showed me alternative ways to solve it. I was horrible in math and science but now I have an a in both subjects. Thanks for the help🤍🤍

David K

iOS user

The app's just great! All I have to do is enter the topic in the search bar and I get the response real fast. I don't have to watch 10 YouTube videos to understand something, so I'm saving my time. Highly recommended!

Sudenaz Ocak

Android user

In school I was really bad at maths but thanks to the app, I am doing better now. I am so grateful that you made the app.

Greenlight Bonnie

Android user

I found this app a couple years ago and it has only gotten better since then. I really love it because it can help with written questions and photo questions. Also, it can find study guides that other people have made as well as flashcard sets and practice tests. The free version is also amazing for students who might not be able to afford it. Would 100% recommend

Aubrey

iOS user

Best app if you're in Highschool or Junior high. I have been using this app for 2 school years and it's the best, it's good if you don't have anyone to help you with school work.😋🩷🎀

Marco B

iOS user

THE QUIZES AND FLASHCARDS ARE SO USEFUL AND I LOVE Knowunity AI. IT ALSO IS LITREALLY LIKE CHATGPT BUT SMARTER!! HELPED ME WITH MY MASCARA PROBLEMS TOO!! AS WELL AS MY REAL SUBJECTS ! DUHHH 😍😁😲🤑💗✨🎀😮

Elisha

iOS user

This app is phenomenal down to the correct info and the various topics you can study! I greatly recommend it for people who struggle with procrastination and those who need homework help. It has been perfectly accurate for world 1 history as far as I’ve seen! Geometry too!

Paul T

iOS user

Pasindi Lahandapurage

@pasindilahandapurage_kqvo

Understanding how economies work helps us make better decisions about resources and money.

Economics AS level notes on factors of productioncovers the four main building blocks of any economy: land (natural resources), labor (human work), capital (tools and equipment),... Show more

Access to all documents

Improve your grades

Join milions of students

The foundation of economics centers on managing scarce resources effectively in a world of unlimited wants. When studying Economics AS level notes on factors of production, it's crucial to understand how resources are allocated among competing uses.

The four fundamental factors of production form the backbone of economic activity. Land encompasses all natural resources like oil, minerals, and agricultural land. Labor represents the human workforce, including both skilled and unskilled workers. Capital consists of man-made tools and equipment used in production . Entrepreneurship provides the crucial element of risk-taking and organizational capability needed to combine these factors effectively.

Definition: Factors of Production are the resource inputs available in an economy for producing goods and services. These include land, labor, capital, and entrepreneurship.

Understanding how households make economic decisions is vital for grasping both microeconomics and macroeconomics household decisions. Households must constantly make choices about consumption, saving, and resource allocation, all while facing the constraint of scarcity.

Access to all documents

Improve your grades

Join milions of students

The economic problem of scarcity necessitates making choices about how to use limited resources. Every economic decision involves an opportunity cost - the next best alternative that must be foregone. This fundamental concept shapes how individuals, businesses, and nations make decisions.

Highlight: Factor endowments - the stock of factors of production available to an economy - significantly influence a country's economic potential and development path.

Production involves transforming inputs into outputs of goods (tangible products) and services (intangible products). The quality and quantity of factor endowments largely determine a country's productive capacity and economic prosperity.

Understanding these relationships helps explain why some nations prosper while others struggle. Countries with abundant and high-quality factor endowments generally have greater productive potential and economic opportunities.

Access to all documents

Improve your grades

Join milions of students

International specialisation advantages and disadvantages play a crucial role in global economic development. When countries specialize in producing goods and services where they have a comparative advantage, it leads to increased efficiency and output.

Example: A country with abundant fertile land might specialize in agricultural products, while another with highly skilled labor might focus on technological products.

However, specialization carries risks. Weather-dependent industries can face severe disruptions from natural disasters. Over-specialization can lead to de-industrialization in some sectors. Additionally, changing consumer preferences or depleting resources can create economic hardships for specialized economies.

The key to successful international specialization lies in balancing the benefits of increased productivity and expanded trade opportunities against the risks of over-dependence on specific sectors or resources.

Access to all documents

Improve your grades

Join milions of students

The Production Possibility Curve (PPC) illustrates the maximum output combinations an economy can achieve with its current resources and technology. This concept helps understand productive efficiency, allocative efficiency, and economic growth.

Vocabulary: Productive efficiency occurs at any point on the PPC, while allocative efficiency involves choosing the optimal combination of goods to produce.

Economic growth, represented by an outward shift of the PPC, can occur through various means. Quantitative growth happens when there's an increase in resource availability, such as through population growth or capital accumulation. Qualitative growth occurs through technological advancement and improved resource quality, such as better education and training.

Understanding these concepts helps explain how economies can expand their productive capacity and achieve sustainable growth over time.

Access to all documents

Improve your grades

Join milions of students

Natural disasters significantly impact a nation's production capabilities, which can be clearly illustrated through Production Possibility Curves (PPC). When examining how events like earthquakes and tsunamis affect production, we see a distinct leftward shift in the PPC, indicating reduced production capacity across all sectors.

The relationship between different sectors, such as manufacturing and agriculture, demonstrates how natural disasters create widespread economic disruption. When resources become constrained due to catastrophic events, the economy's ability to produce different combinations of goods diminishes uniformly, resulting in the entire PPC shifting inward.

Definition: A Production Possibility Curve (PPC) represents the maximum possible production combinations of two goods that an economy can achieve with its available resources.

Understanding imperfect substitutes is crucial when analyzing PPC shifts. The curved nature of the PPC, rather than a straight line, indicates that resources cannot be perfectly substituted between different production processes. This reflects real-world limitations in resource allocation and production flexibility.

Access to all documents

Improve your grades

Join milions of students

Economic systems serve as the fundamental framework determining how societies allocate their resources. In Microeconomics and macroeconomics household decisions play a crucial role in shaping these systems, whether in market economies, command economies, or mixed economic systems.

Market economies operate through the price system, where supply and demand forces determine resource allocation. Command economies, conversely, rely on central planning and state ownership. Mixed economies combine elements of both systems, allowing for both market forces and government intervention.

Highlight: The price system in market economies serves as an automatic mechanism for resource allocation, while command economies rely on centralized planning decisions.

These different economic systems each present unique advantages and challenges in addressing the fundamental economic questions of what to produce, how to produce it, and for whom to produce. The effectiveness of each system depends on various factors including social goals, resource availability, and technological capabilities.

Access to all documents

Improve your grades

Join milions of students

Free market economies excel in promoting innovation and efficiency through competition. They provide consumer choice and typically generate higher economic growth rates compared to command economies. However, they may struggle with providing public goods and addressing income inequality.

Command economies, while often criticized for inefficiency, can better ensure the provision of public goods and maintain more equitable income distribution. They can also implement environmental protection measures more directly, though often at the cost of reduced economic dynamism.

Example: In a free market economy, private companies might underinvest in public transportation infrastructure, while a command economy can directly allocate resources to such projects regardless of immediate profitability.

The debate between these systems highlights the fundamental tradeoffs between efficiency and equity, innovation and stability, individual freedom and collective planning. Understanding these tradeoffs is crucial for evaluating economic policy decisions and their societal impacts.

Access to all documents

Improve your grades

Join milions of students

International specialisation advantages and disadvantages significantly impact both firms and workers in the modern global economy. Specialization increases productivity and efficiency through focused expertise development and the use of specialized machinery.

For firms, specialization enables increased output, improved quality, and potential economies of scale. Workers benefit from higher wages in specialized roles and enhanced skill development in their specific areas. However, both parties face certain risks and limitations.

Vocabulary: Division of Labor refers to the breakdown of production processes into specialized tasks, enabling increased efficiency but potentially leading to worker monotony.

The disadvantages include reduced flexibility for firms and potential worker boredom from repetitive tasks. Firms may face higher training costs and dependence on specific suppliers, while workers risk skill degradation in other areas and possible technological replacement. Understanding these tradeoffs is essential for businesses making organizational decisions and workers planning their career development.

Access to all documents

Improve your grades

Join milions of students

Consumer and producer surplus are fundamental concepts in Economics AS level notes on factors of production that help us understand market efficiency and welfare. These concepts illustrate how both buyers and sellers benefit from market transactions.

Consumer surplus represents the economic benefit buyers receive when they purchase a product for less than what they were willing to pay. When market prices decrease, consumer surplus increases, creating greater economic value for buyers. This relationship demonstrates how price changes directly impact consumer welfare and purchasing decisions in Microeconomics and macroeconomics household decisions.

Producer surplus occurs when sellers receive more for their products than the minimum amount they would have accepted. This concept is crucial for understanding market dynamics and how prices affect business profitability. When analyzing producer surplus, we must consider supply curve elasticity and market price fluctuations to determine the total economic benefit producers receive.

Definition: Consumer surplus is the difference between what consumers are willing to pay and what they actually pay, while producer surplus is the difference between what producers receive and their minimum acceptable price.

Example: If a consumer is willing to pay $10 for a book but only pays $7, their consumer surplus is $3. Similarly, if a producer would accept $5 for the book but sells it for $7, their producer surplus is $2.

Access to all documents

Improve your grades

Join milions of students

Price changes significantly impact both consumer and producer surplus, demonstrating key principles of International specialisation advantages and disadvantages. When prices decrease, consumer surplus typically increases as buyers can purchase goods for less than their maximum willingness to pay. This creates additional economic value and increases overall market efficiency.

The magnitude of changes in consumer and producer surplus depends on several factors, including the elasticity of demand and supply curves. Steeper curves result in larger surplus changes when prices shift, while flatter curves lead to smaller changes. This relationship helps economists analyze market outcomes and predict the distribution of economic benefits.

Understanding these surplus concepts is essential for analyzing market efficiency and policy impacts. When evaluating market interventions or price controls, economists consider how changes affect both consumer and producer surplus to determine overall economic welfare effects.

Highlight: The size of surplus changes depends on:

Our AI companion is specifically built for the needs of students. Based on the millions of content pieces we have on the platform we can provide truly meaningful and relevant answers to students. But its not only about answers, the companion is even more about guiding students through their daily learning challenges, with personalised study plans, quizzes or content pieces in the chat and 100% personalisation based on the students skills and developments.

You can download the app in the Google Play Store and in the Apple App Store.

That's right! Enjoy free access to study content, connect with fellow students, and get instant help – all at your fingertips.

5

Smart Tools NEW

Transform this note into: ✓ 50+ Practice Questions ✓ Interactive Flashcards ✓ Full Practice Test ✓ Essay Outlines

Project Bibliography

Notes from Contract Law for 1L students

Fishery Laws

Chapter One The Homicide Crime Scene Lecture Notes

This will help with what you need to know before you go into an interview.

Different family dynamics typical and atypical

App Store

Google Play

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan S

iOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha Klich

Android user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

Anna

iOS user

I think it’s very much worth it and you’ll end up using it a lot once you get the hang of it and even after looking at others notes you can still ask your Artificial intelligence buddy the question and ask to simplify it if you still don’t get it!!! In the end I think it’s worth it 😊👍 ⚠️Also DID I MENTION ITS FREEE YOU DON’T HAVE TO PAY FOR ANYTHING AND STILL GET YOUR GRADES IN PERFECTLY❗️❗️⚠️

Thomas R

iOS user

Knowunity is the BEST app I’ve used in a minute. This is not an ai review or anything this is genuinely coming from a 7th grade student (I know 2011 im young) but dude this app is a 10/10 i have maintained a 3.8 gpa and have plenty of time for gaming. I love it and my mom is just happy I got good grades

Brad T

Android user

Not only did it help me find the answer but it also showed me alternative ways to solve it. I was horrible in math and science but now I have an a in both subjects. Thanks for the help🤍🤍

David K

iOS user

The app's just great! All I have to do is enter the topic in the search bar and I get the response real fast. I don't have to watch 10 YouTube videos to understand something, so I'm saving my time. Highly recommended!

Sudenaz Ocak

Android user

In school I was really bad at maths but thanks to the app, I am doing better now. I am so grateful that you made the app.

Greenlight Bonnie

Android user

I found this app a couple years ago and it has only gotten better since then. I really love it because it can help with written questions and photo questions. Also, it can find study guides that other people have made as well as flashcard sets and practice tests. The free version is also amazing for students who might not be able to afford it. Would 100% recommend

Aubrey

iOS user

Best app if you're in Highschool or Junior high. I have been using this app for 2 school years and it's the best, it's good if you don't have anyone to help you with school work.😋🩷🎀

Marco B

iOS user

THE QUIZES AND FLASHCARDS ARE SO USEFUL AND I LOVE Knowunity AI. IT ALSO IS LITREALLY LIKE CHATGPT BUT SMARTER!! HELPED ME WITH MY MASCARA PROBLEMS TOO!! AS WELL AS MY REAL SUBJECTS ! DUHHH 😍😁😲🤑💗✨🎀😮

Elisha

iOS user

This app is phenomenal down to the correct info and the various topics you can study! I greatly recommend it for people who struggle with procrastination and those who need homework help. It has been perfectly accurate for world 1 history as far as I’ve seen! Geometry too!

Paul T

iOS user

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan S

iOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha Klich

Android user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

Anna

iOS user

I think it’s very much worth it and you’ll end up using it a lot once you get the hang of it and even after looking at others notes you can still ask your Artificial intelligence buddy the question and ask to simplify it if you still don’t get it!!! In the end I think it’s worth it 😊👍 ⚠️Also DID I MENTION ITS FREEE YOU DON’T HAVE TO PAY FOR ANYTHING AND STILL GET YOUR GRADES IN PERFECTLY❗️❗️⚠️

Thomas R

iOS user

Knowunity is the BEST app I’ve used in a minute. This is not an ai review or anything this is genuinely coming from a 7th grade student (I know 2011 im young) but dude this app is a 10/10 i have maintained a 3.8 gpa and have plenty of time for gaming. I love it and my mom is just happy I got good grades

Brad T

Android user

Not only did it help me find the answer but it also showed me alternative ways to solve it. I was horrible in math and science but now I have an a in both subjects. Thanks for the help🤍🤍

David K

iOS user

The app's just great! All I have to do is enter the topic in the search bar and I get the response real fast. I don't have to watch 10 YouTube videos to understand something, so I'm saving my time. Highly recommended!

Sudenaz Ocak

Android user

In school I was really bad at maths but thanks to the app, I am doing better now. I am so grateful that you made the app.

Greenlight Bonnie

Android user

I found this app a couple years ago and it has only gotten better since then. I really love it because it can help with written questions and photo questions. Also, it can find study guides that other people have made as well as flashcard sets and practice tests. The free version is also amazing for students who might not be able to afford it. Would 100% recommend

Aubrey

iOS user

Best app if you're in Highschool or Junior high. I have been using this app for 2 school years and it's the best, it's good if you don't have anyone to help you with school work.😋🩷🎀

Marco B

iOS user

THE QUIZES AND FLASHCARDS ARE SO USEFUL AND I LOVE Knowunity AI. IT ALSO IS LITREALLY LIKE CHATGPT BUT SMARTER!! HELPED ME WITH MY MASCARA PROBLEMS TOO!! AS WELL AS MY REAL SUBJECTS ! DUHHH 😍😁😲🤑💗✨🎀😮

Elisha

iOS user

This app is phenomenal down to the correct info and the various topics you can study! I greatly recommend it for people who struggle with procrastination and those who need homework help. It has been perfectly accurate for world 1 history as far as I’ve seen! Geometry too!

Paul T

iOS user