Economics is the study of how we produce and exchange...

Comprehensive AP Macroeconomics Unit 1 Study Notes

Dev@rip_tide

1 / 7

1

of 7

Basic Economic Concepts

Economics deals with the challenge of scarcity - having unlimited wants but limited resources. This creates the need to make choices about how to allocate what we have.

The economy relies on three main factors of production: land (physical space and natural resources), labor (human work), and capital (tools, machinery, and buildings used to produce goods). These resources are used to create either consumer goods (products for direct use) or capital goods (resources businesses use to produce consumer goods).

Resource allocation refers to how societies distribute scarce resources. This distribution process is central to understanding different economic systems and how they function.

💡 Think of economics as the study of choices: every time you spend money on one thing, you're choosing not to spend it on something else. This trade-off is at the heart of economic thinking!

2

of 7

Economic Systems & Opportunity Cost

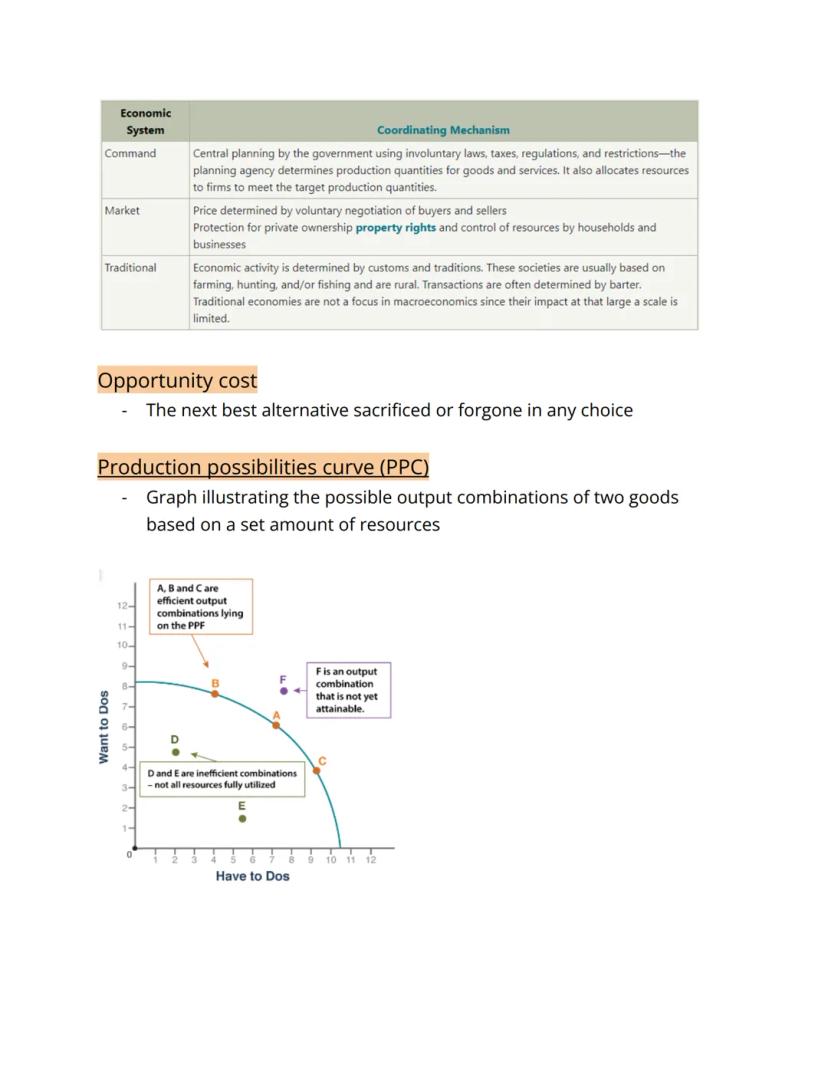

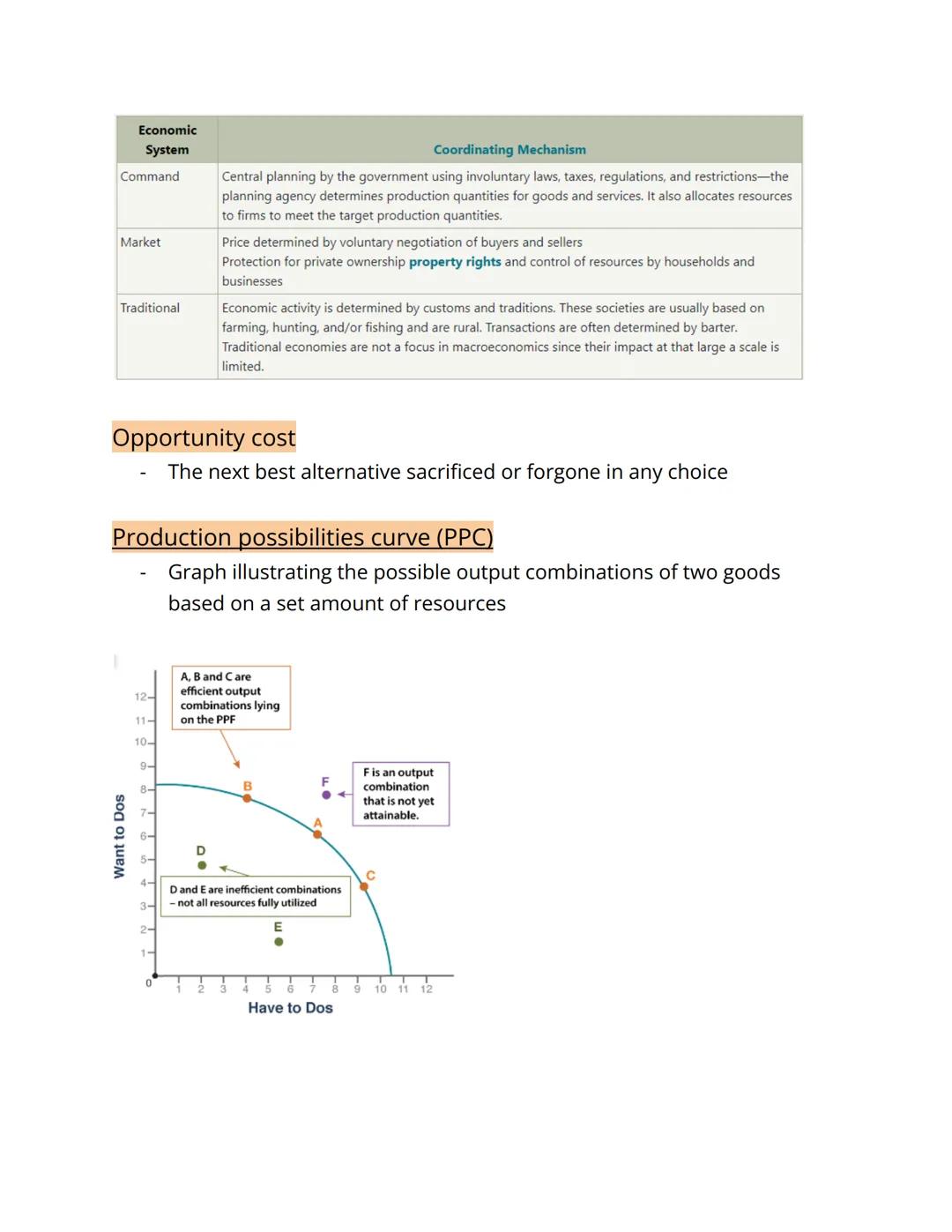

Different societies organize their economies in different ways. A command economy uses central government planning to decide what gets produced. A market economy relies on prices and voluntary exchanges between buyers and sellers, with protection for private property rights. Traditional economies base economic decisions on customs and traditions.

The concept of opportunity cost is crucial in economics - it's the next best alternative you give up when making a choice. For example, if you spend an hour studying economics, your opportunity cost might be an hour of sleep or socializing.

The production possibilities curve (PPC) shows different combinations of goods an economy can produce with its available resources. Points on the curve (like A, B, C) represent efficient production, while points inside the curve (like D, E) show inefficient use of resources. Points beyond the curve (like F) represent combinations not yet attainable with current resources.

💡 Every economic decision comes with a trade-off! Understanding opportunity cost helps you make better choices about how to use your limited time, money, and resources.

3

of 7

Types of Opportunity Cost

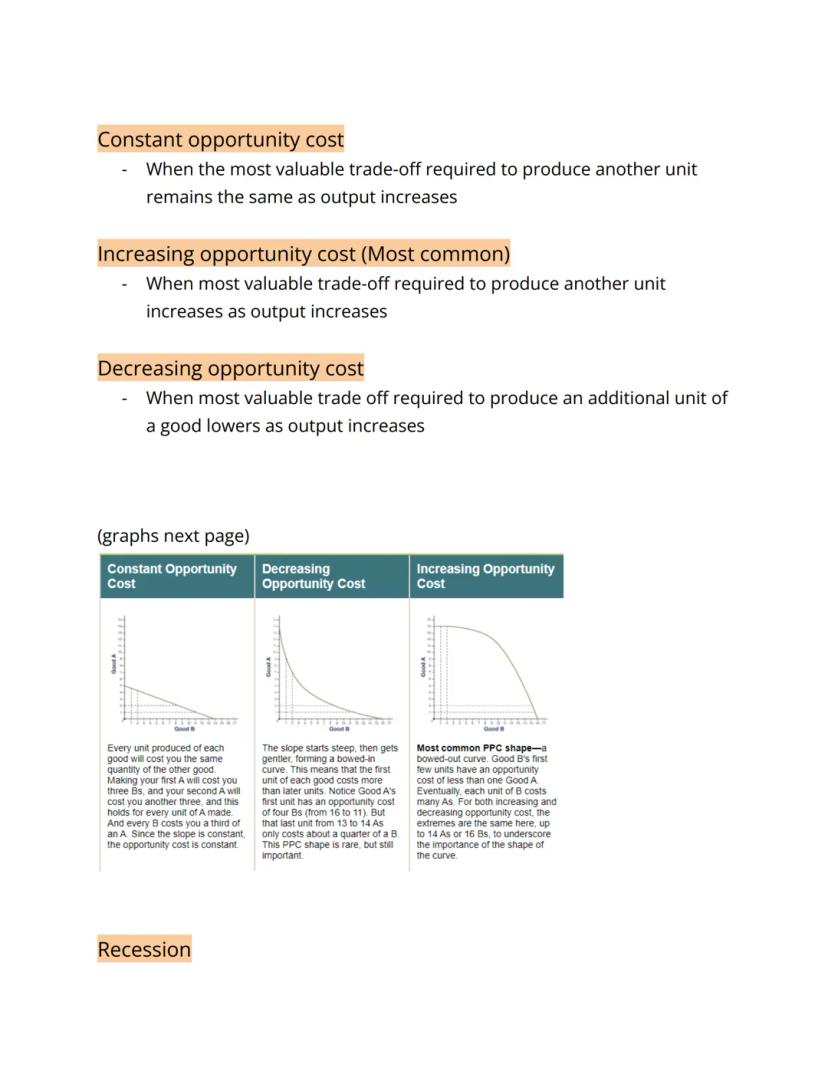

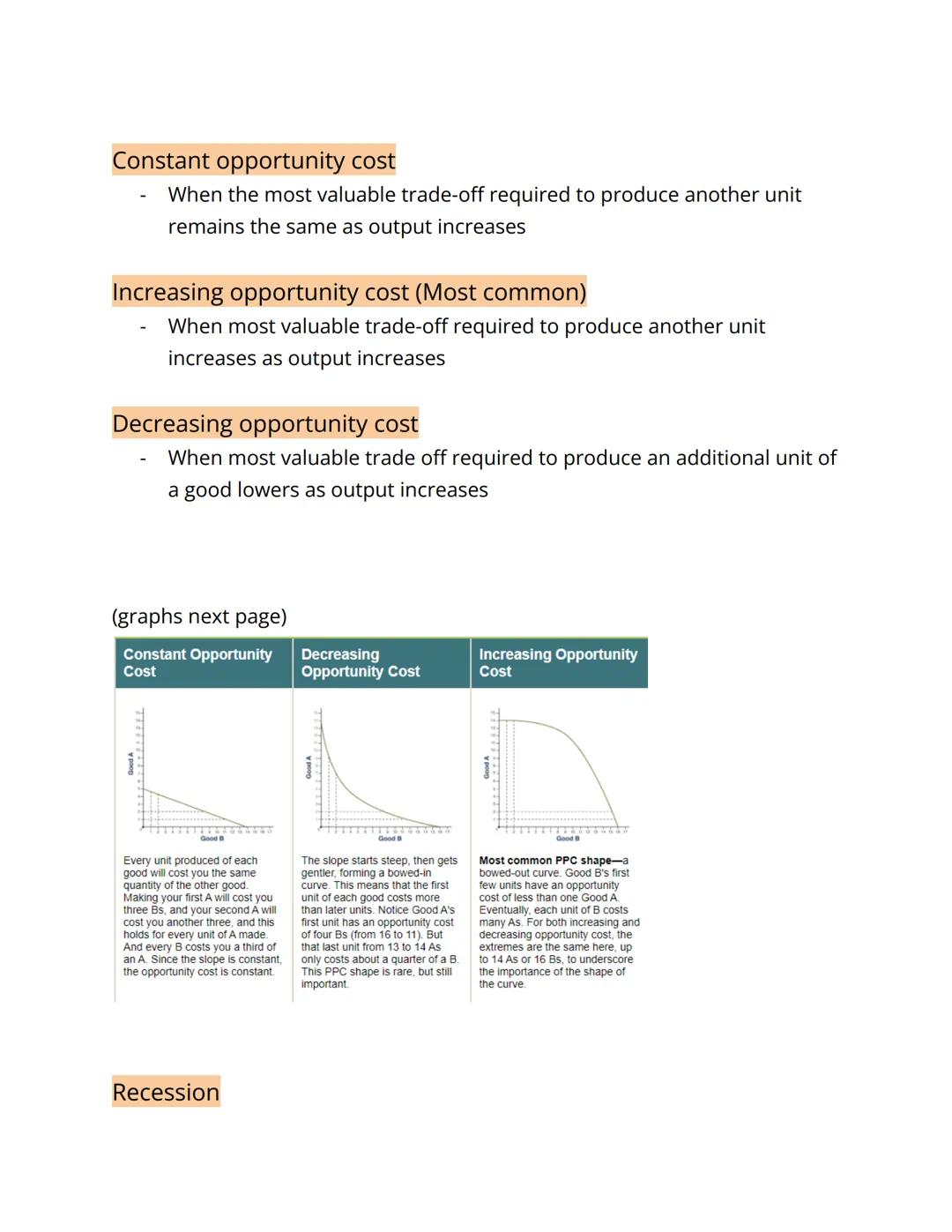

The shape of a PPC reveals important information about opportunity costs in an economy. There are three main types:

With constant opportunity cost, the trade-off stays the same no matter how much you produce. The PPC appears as a straight line. For example, if producing one unit of Good A always costs exactly three units of Good B, the opportunity cost is constant.

Increasing opportunity cost is most common in real economies. As you produce more of one good, you give up increasingly more of another. This creates a bowed-out curve. Initially, you sacrifice less of Good A to get more of Good B, but eventually, each additional unit of Good B requires giving up many units of Good A.

Decreasing opportunity cost is rare but important. It creates a bowed-in curve where the first units produced have a higher opportunity cost than later units. Production becomes more efficient as you specialize.

💡 Most real-world production follows the increasing opportunity cost model – this explains why economies can't simply produce unlimited amounts of everything we want!

4

of 7

Economic Change & Trade Advantages

A recession represents a significant economic downturn where resources become underutilized - meaning land, labor, and capital aren't being used to their maximum productivity. This leads to economic contraction, a decrease in society's ability to produce goods and services.

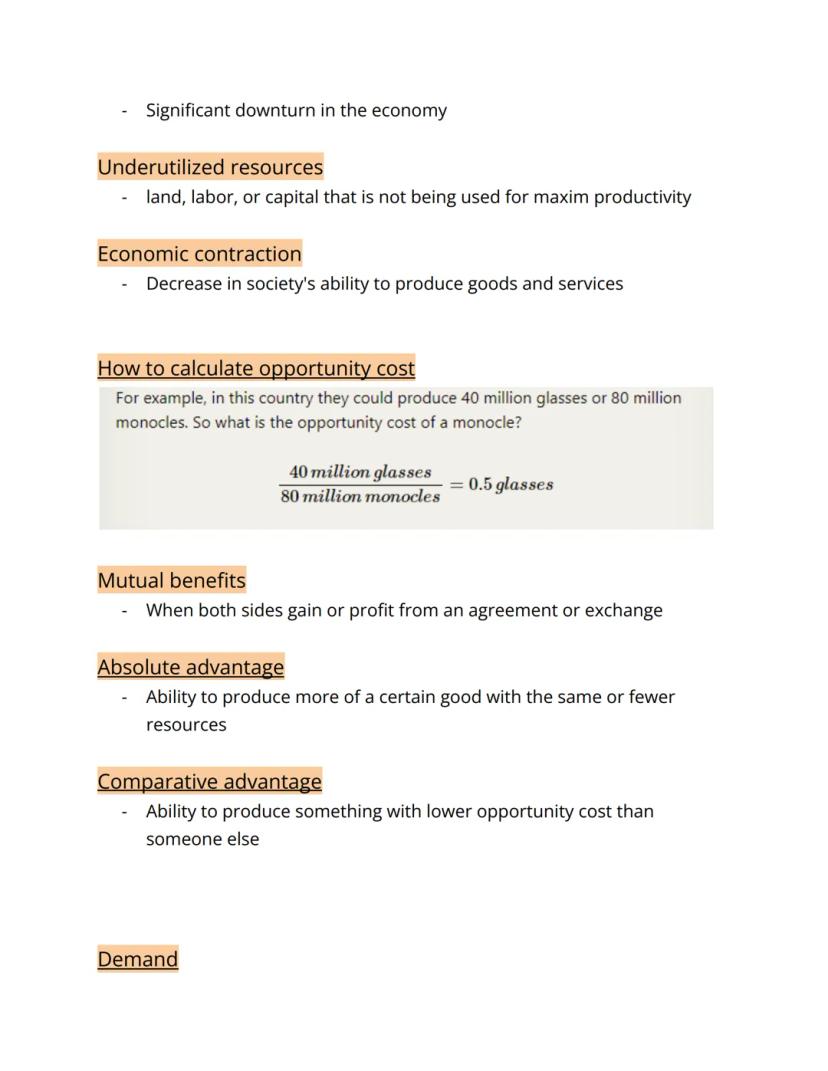

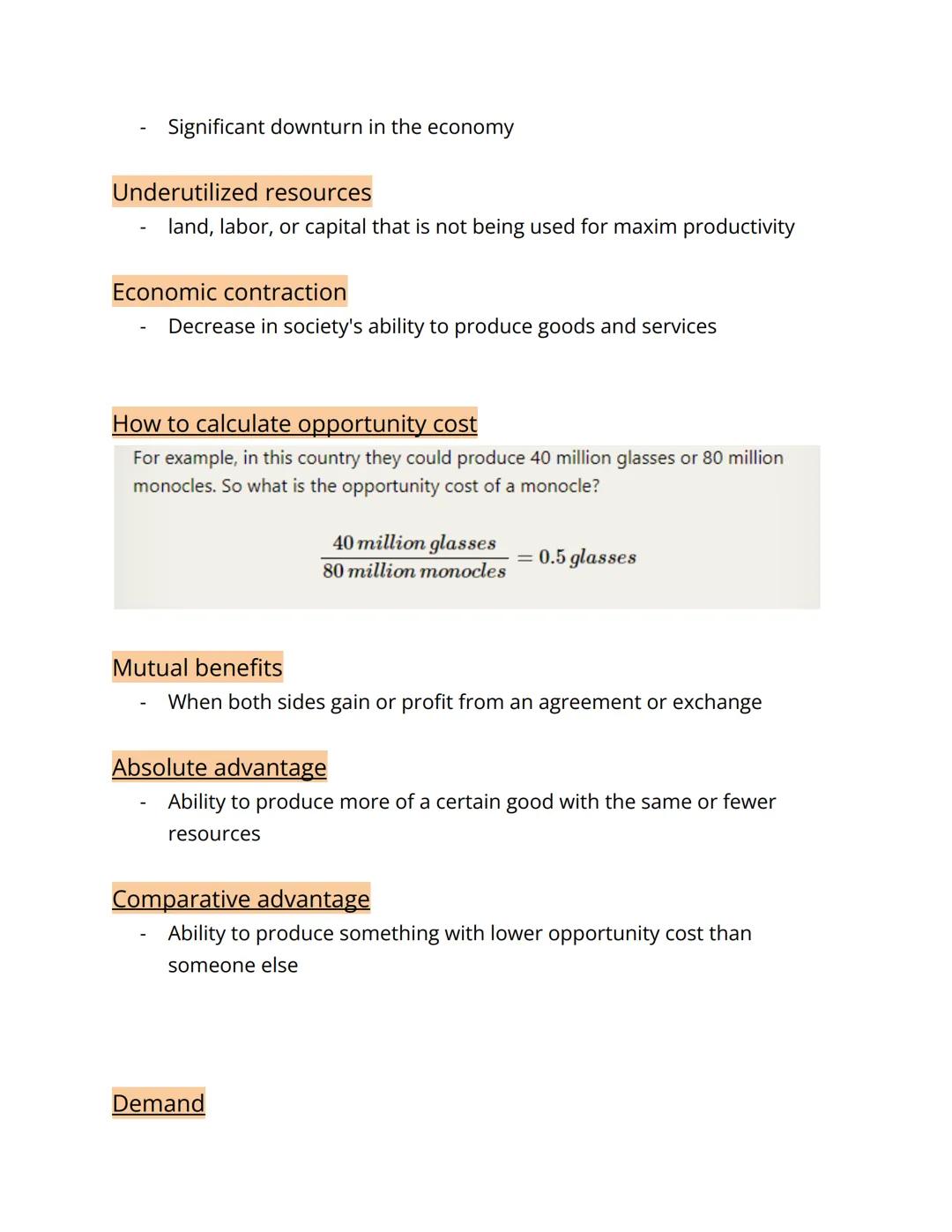

You can calculate opportunity cost mathematically. For example, if a country can produce either 40 million glasses or 80 million monocles, the opportunity cost of one monocle is 0.5 glasses (40 million glasses ÷ 80 million monocles = 0.5).

Trade between countries works because it creates mutual benefits where both sides gain from the exchange. Countries may have different advantages:

- An absolute advantage means being able to produce more goods with the same or fewer resources

- A comparative advantage means being able to produce something with a lower opportunity cost than others

💡 Understanding comparative advantage explains why countries trade even when one country seems better at producing everything – it's about opportunity costs, not just productivity!

5

of 7

Demand & Market Basics

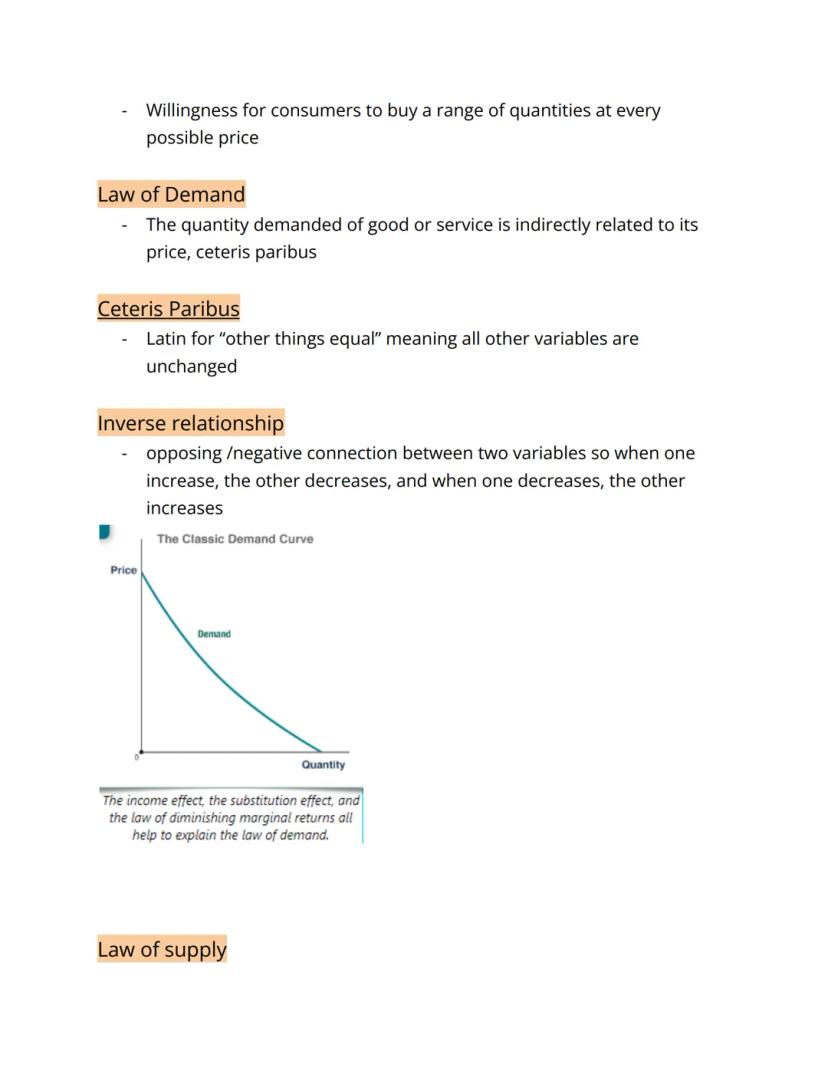

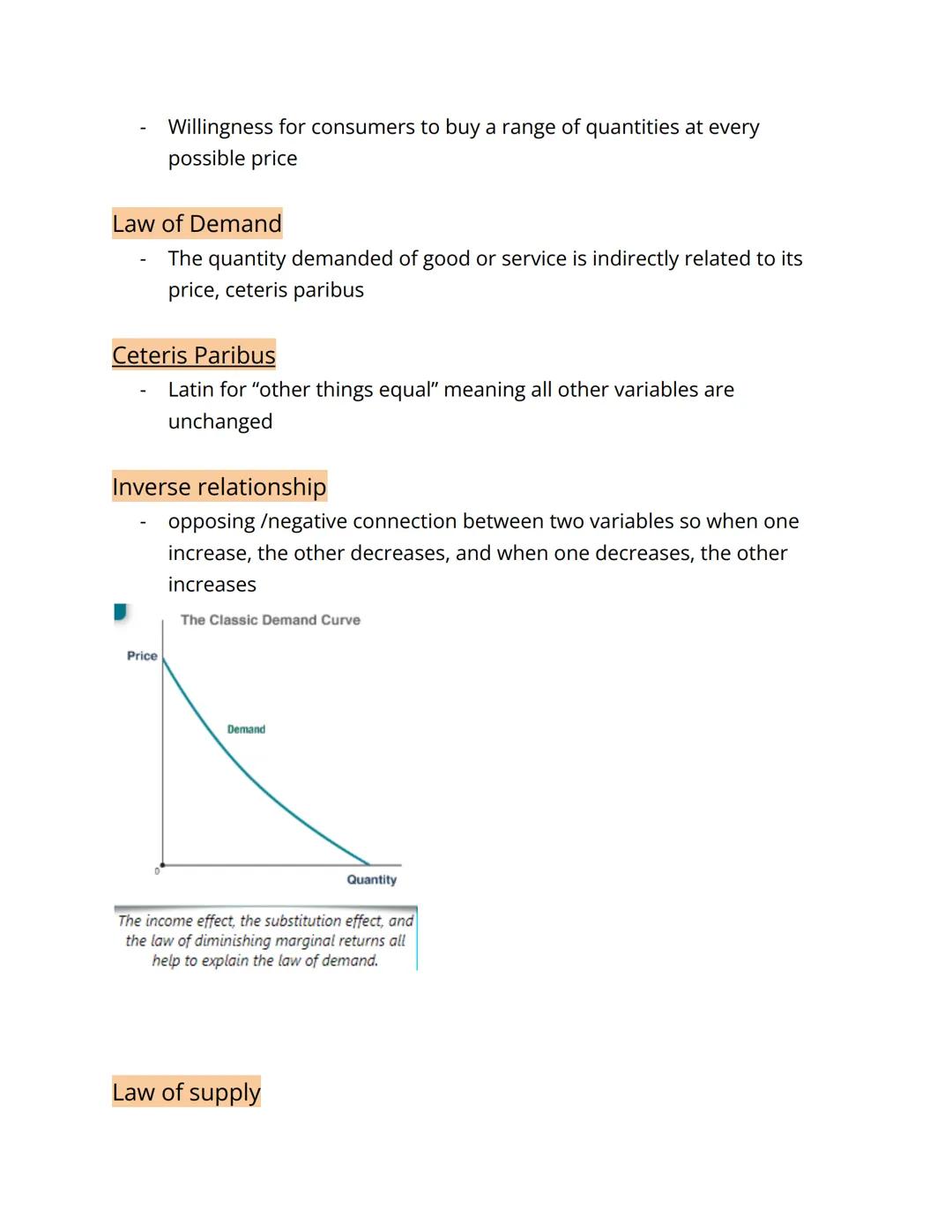

Demand represents consumers' willingness to buy different quantities of a good at various prices. The Law of Demand states that quantity demanded is inversely related to price, ceteris paribus (all other factors remaining equal).

This creates an inverse relationship between price and quantity demanded – as prices rise, people buy less, and as prices fall, people buy more. This fundamental economic principle is why demand curves slope downward.

The classic demand curve shows this relationship visually. Several factors explain this behavior: the income effect (higher prices reduce purchasing power), the substitution effect (people switch to alternatives when prices rise), and diminishing marginal returns (each additional unit provides less satisfaction).

💡 Next time you see a sale, think about the Law of Demand in action! When prices drop, people naturally want to buy more – that's why stores use discounts to clear inventory.

6

of 7

Supply & Market Equilibrium

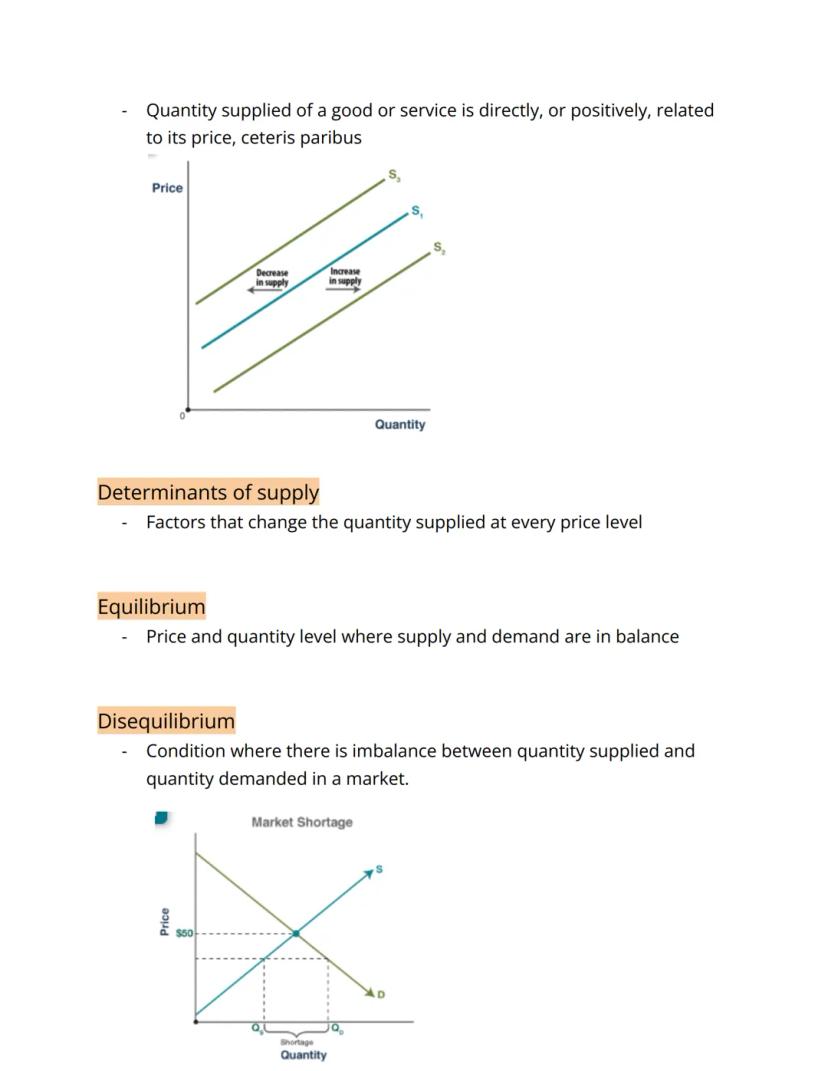

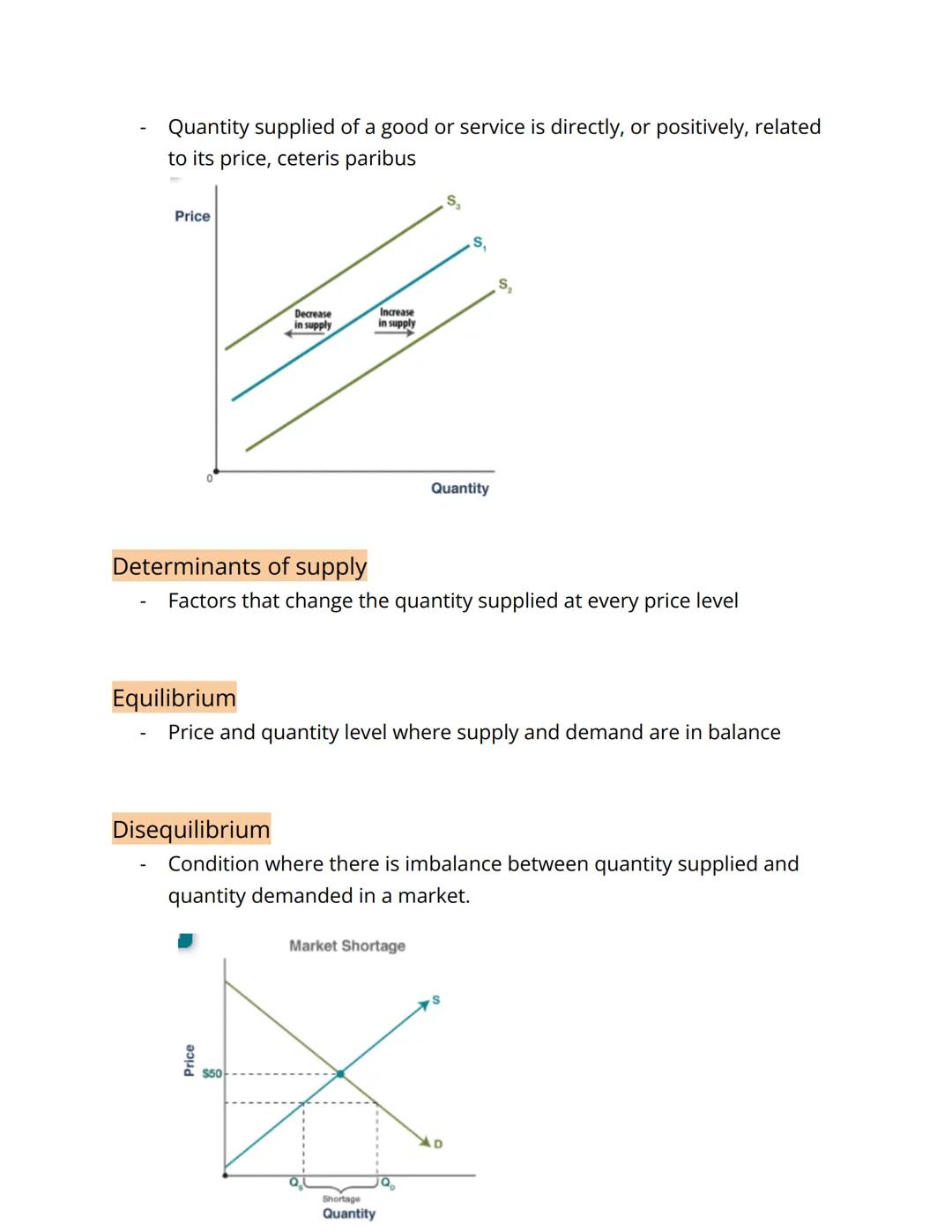

The Law of Supply states that quantity supplied increases as price increases (ceteris paribus). Unlike demand, this creates a direct or positive relationship between price and quantity. Supply curves slope upward because producers are willing to make more when they can sell at higher prices.

Various determinants of supply (like technology, input costs, and government policies) can shift the entire supply curve left or right. This changes the quantity suppliers are willing to offer at every price level.

Equilibrium occurs at the price and quantity where supply and demand are perfectly balanced. When markets aren't in balance, they're in disequilibrium, which can lead to shortages (when demand exceeds supply) or surpluses (when supply exceeds demand).

💡 Markets naturally move toward equilibrium! When there's a shortage, prices rise, encouraging more production while discouraging some consumption until balance is restored.

7

of 7

Price Controls & Market Shifts

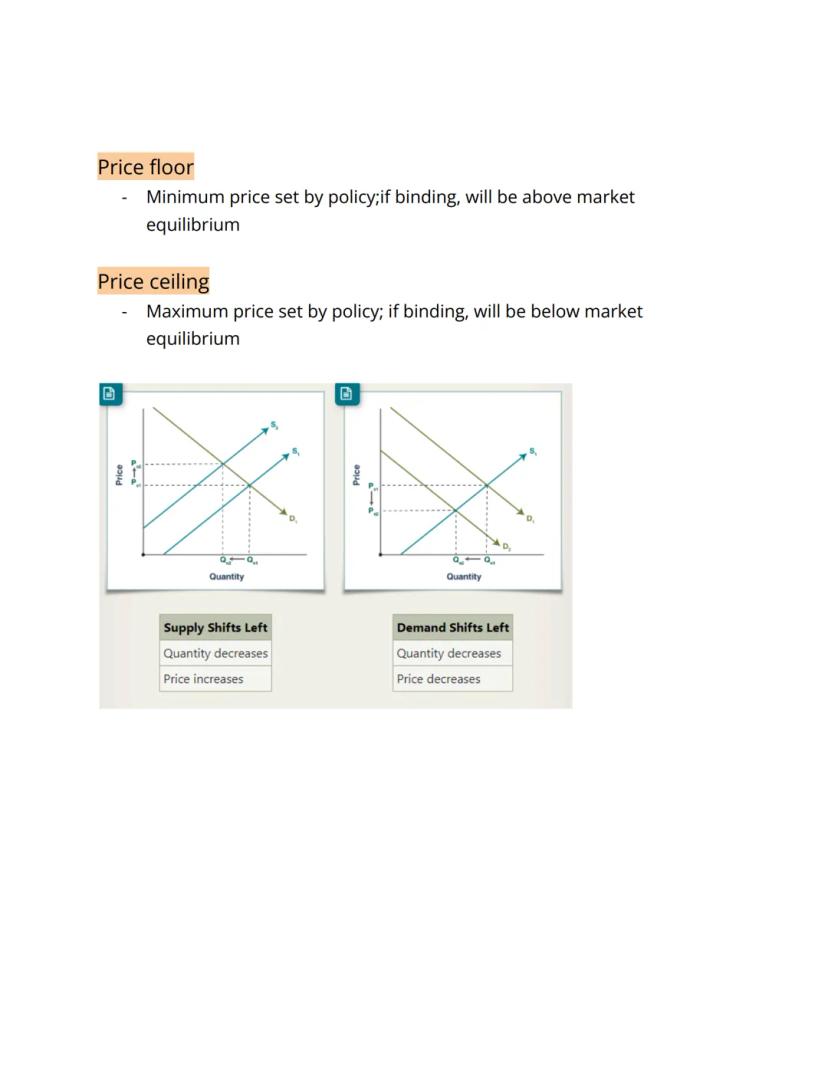

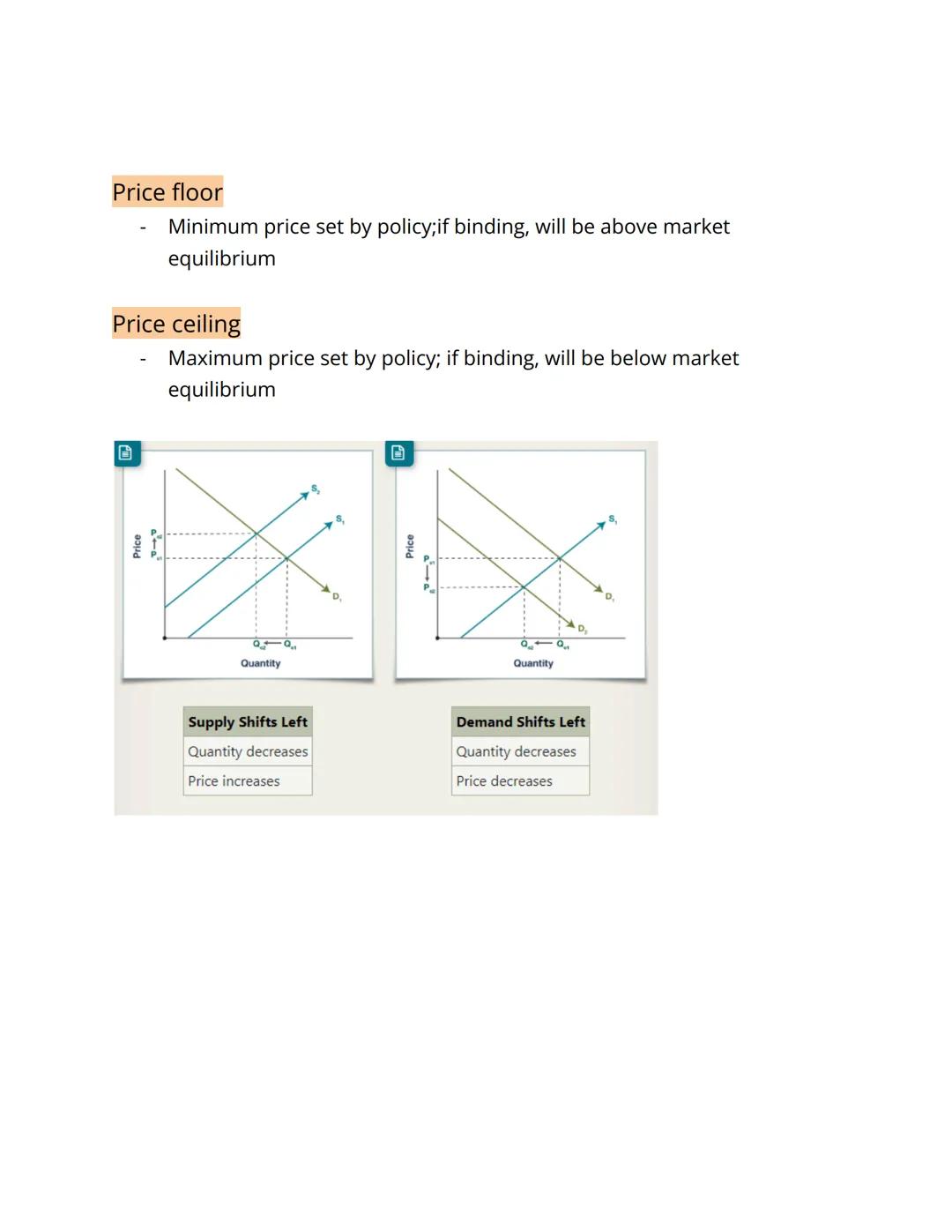

Governments sometimes implement price controls to influence markets. A price floor sets a minimum price (like minimum wage) that must be above equilibrium to have effect. A price ceiling establishes a maximum price (like rent control) that must be below equilibrium to impact the market.

When supply shifts left (decreases), two things happen: quantity decreases and price increases. This might occur due to resource shortages, higher production costs, or new regulations.

When demand shifts left (decreases), both quantity and price decrease. This could result from changing consumer preferences, lower incomes, or cheaper substitute products becoming available.

💡 Understanding market shifts helps explain everyday economic changes! When gas prices spike after a pipeline issue, that's a leftward shift in supply. When vacation rentals get cheaper in the off-season, that's a leftward shift in demand.

We thought you’d never ask...

Our AI companion is specifically built for the needs of students. Based on the millions of content pieces we have on the platform we can provide truly meaningful and relevant answers to students. But its not only about answers, the companion is even more about guiding students through their daily learning challenges, with personalised study plans, quizzes or content pieces in the chat and 100% personalisation based on the students skills and developments.

You can download the app in the Google Play Store and in the Apple App Store.

That's right! Enjoy free access to study content, connect with fellow students, and get instant help – all at your fingertips.

Similar Content

Most popular content in AP Macroeconomics

4Most popular content

9O

Origins and Dynamics of the Columbian Exchange

Analyze the ecological and economic motivations behind the initial transfer of goods, people, and diseases between the Old and New Worlds.

9th3,1280

I

Introduction to Early Cultural Interactions

Analyze the initial social and religious encounters between Europeans, Africans, and Indigenous peoples in the colonial Americas.

9th2,7730

O

Origins of Ancient River Civilizations

Analyze the environmental factors and technological innovations that led to the rise of early states in Mesopotamia, Egypt, and the Indus Valley.

9th3,1870

M

Motivations for European Exploration

Analyze the economic, religious, and political factors that drove European powers to the Americas during the 15th and 16th centuries.

9th1,7780

F

Foundations of Ethical Guidelines in Research

Practice the core principles of the APA ethical code including informed consent, debriefing, and the role of Institutional Review Boards.

9th1,3360

I

Introduction to Native American Societies

Examine the diverse social, political, and economic structures of North American indigenous groups prior to European contact.

9th1,1100

I

Introduction to the Spanish Encomienda System

Explore the fundamental economic and social structures of the Spanish colonial system, focusing on the encomienda and the casta social hierarchy.

9th8890

I

Introduction to Biological Elements of Life

Practice identifying the essential elements including carbon, nitrogen, phosphorus, and sulfur that compose biological macromolecules.

9th1,7410

O

Origins of the Articles of Confederation

Practice identifying the motivations for a weak central government and the specific powers granted to the states under the first U.S. constitution.

9th9370

Students love us — and so will you.

4.6/5App Store

4.7/5Google Play

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan SiOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha KlichAndroid user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

AnnaiOS user

Comprehensive AP Macroeconomics Unit 1 Study Notes

Dev@rip_tide

Economics is the study of how we produce and exchange goods and services in a world of scarcity. Understanding economic concepts helps explain how markets work, why prices change, and how societies distribute limited resources. These fundamentals form the backbone...

1

of 7

Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Basic Economic Concepts

Economics deals with the challenge of scarcity - having unlimited wants but limited resources. This creates the need to make choices about how to allocate what we have.

The economy relies on three main factors of production: land (physical space and natural resources), labor (human work), and capital (tools, machinery, and buildings used to produce goods). These resources are used to create either consumer goods (products for direct use) or capital goods (resources businesses use to produce consumer goods).

Resource allocation refers to how societies distribute scarce resources. This distribution process is central to understanding different economic systems and how they function.

💡 Think of economics as the study of choices: every time you spend money on one thing, you're choosing not to spend it on something else. This trade-off is at the heart of economic thinking!

2

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Economic Systems & Opportunity Cost

Different societies organize their economies in different ways. A command economy uses central government planning to decide what gets produced. A market economy relies on prices and voluntary exchanges between buyers and sellers, with protection for private property rights. Traditional economies base economic decisions on customs and traditions.

The concept of opportunity cost is crucial in economics - it's the next best alternative you give up when making a choice. For example, if you spend an hour studying economics, your opportunity cost might be an hour of sleep or socializing.

The production possibilities curve (PPC) shows different combinations of goods an economy can produce with its available resources. Points on the curve (like A, B, C) represent efficient production, while points inside the curve (like D, E) show inefficient use of resources. Points beyond the curve (like F) represent combinations not yet attainable with current resources.

💡 Every economic decision comes with a trade-off! Understanding opportunity cost helps you make better choices about how to use your limited time, money, and resources.

3

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Types of Opportunity Cost

The shape of a PPC reveals important information about opportunity costs in an economy. There are three main types:

With constant opportunity cost, the trade-off stays the same no matter how much you produce. The PPC appears as a straight line. For example, if producing one unit of Good A always costs exactly three units of Good B, the opportunity cost is constant.

Increasing opportunity cost is most common in real economies. As you produce more of one good, you give up increasingly more of another. This creates a bowed-out curve. Initially, you sacrifice less of Good A to get more of Good B, but eventually, each additional unit of Good B requires giving up many units of Good A.

Decreasing opportunity cost is rare but important. It creates a bowed-in curve where the first units produced have a higher opportunity cost than later units. Production becomes more efficient as you specialize.

💡 Most real-world production follows the increasing opportunity cost model – this explains why economies can't simply produce unlimited amounts of everything we want!

4

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Economic Change & Trade Advantages

A recession represents a significant economic downturn where resources become underutilized - meaning land, labor, and capital aren't being used to their maximum productivity. This leads to economic contraction, a decrease in society's ability to produce goods and services.

You can calculate opportunity cost mathematically. For example, if a country can produce either 40 million glasses or 80 million monocles, the opportunity cost of one monocle is 0.5 glasses (40 million glasses ÷ 80 million monocles = 0.5).

Trade between countries works because it creates mutual benefits where both sides gain from the exchange. Countries may have different advantages:

- An absolute advantage means being able to produce more goods with the same or fewer resources

- A comparative advantage means being able to produce something with a lower opportunity cost than others

💡 Understanding comparative advantage explains why countries trade even when one country seems better at producing everything – it's about opportunity costs, not just productivity!

5

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Demand & Market Basics

Demand represents consumers' willingness to buy different quantities of a good at various prices. The Law of Demand states that quantity demanded is inversely related to price, ceteris paribus (all other factors remaining equal).

This creates an inverse relationship between price and quantity demanded – as prices rise, people buy less, and as prices fall, people buy more. This fundamental economic principle is why demand curves slope downward.

The classic demand curve shows this relationship visually. Several factors explain this behavior: the income effect (higher prices reduce purchasing power), the substitution effect (people switch to alternatives when prices rise), and diminishing marginal returns (each additional unit provides less satisfaction).

💡 Next time you see a sale, think about the Law of Demand in action! When prices drop, people naturally want to buy more – that's why stores use discounts to clear inventory.

6

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Supply & Market Equilibrium

The Law of Supply states that quantity supplied increases as price increases (ceteris paribus). Unlike demand, this creates a direct or positive relationship between price and quantity. Supply curves slope upward because producers are willing to make more when they can sell at higher prices.

Various determinants of supply (like technology, input costs, and government policies) can shift the entire supply curve left or right. This changes the quantity suppliers are willing to offer at every price level.

Equilibrium occurs at the price and quantity where supply and demand are perfectly balanced. When markets aren't in balance, they're in disequilibrium, which can lead to shortages (when demand exceeds supply) or surpluses (when supply exceeds demand).

💡 Markets naturally move toward equilibrium! When there's a shortage, prices rise, encouraging more production while discouraging some consumption until balance is restored.

7

of 7Sign up to see the content. It's free!

- Access to all documents

- Improve your grades

- Join milions of students

Price Controls & Market Shifts

Governments sometimes implement price controls to influence markets. A price floor sets a minimum price (like minimum wage) that must be above equilibrium to have effect. A price ceiling establishes a maximum price (like rent control) that must be below equilibrium to impact the market.

When supply shifts left (decreases), two things happen: quantity decreases and price increases. This might occur due to resource shortages, higher production costs, or new regulations.

When demand shifts left (decreases), both quantity and price decrease. This could result from changing consumer preferences, lower incomes, or cheaper substitute products becoming available.

💡 Understanding market shifts helps explain everyday economic changes! When gas prices spike after a pipeline issue, that's a leftward shift in supply. When vacation rentals get cheaper in the off-season, that's a leftward shift in demand.

We thought you’d never ask...

Our AI companion is specifically built for the needs of students. Based on the millions of content pieces we have on the platform we can provide truly meaningful and relevant answers to students. But its not only about answers, the companion is even more about guiding students through their daily learning challenges, with personalised study plans, quizzes or content pieces in the chat and 100% personalisation based on the students skills and developments.

You can download the app in the Google Play Store and in the Apple App Store.

That's right! Enjoy free access to study content, connect with fellow students, and get instant help – all at your fingertips.

Similar Content

Most popular content in AP Macroeconomics

4Most popular content

9O

Origins and Dynamics of the Columbian Exchange

Analyze the ecological and economic motivations behind the initial transfer of goods, people, and diseases between the Old and New Worlds.

9th3,1280

I

Introduction to Early Cultural Interactions

Analyze the initial social and religious encounters between Europeans, Africans, and Indigenous peoples in the colonial Americas.

9th2,7730

O

Origins of Ancient River Civilizations

Analyze the environmental factors and technological innovations that led to the rise of early states in Mesopotamia, Egypt, and the Indus Valley.

9th3,1870

M

Motivations for European Exploration

Analyze the economic, religious, and political factors that drove European powers to the Americas during the 15th and 16th centuries.

9th1,7780

F

Foundations of Ethical Guidelines in Research

Practice the core principles of the APA ethical code including informed consent, debriefing, and the role of Institutional Review Boards.

9th1,3360

I

Introduction to Native American Societies

Examine the diverse social, political, and economic structures of North American indigenous groups prior to European contact.

9th1,1100

I

Introduction to the Spanish Encomienda System

Explore the fundamental economic and social structures of the Spanish colonial system, focusing on the encomienda and the casta social hierarchy.

9th8890

I

Introduction to Biological Elements of Life

Practice identifying the essential elements including carbon, nitrogen, phosphorus, and sulfur that compose biological macromolecules.

9th1,7410

O

Origins of the Articles of Confederation

Practice identifying the motivations for a weak central government and the specific powers granted to the states under the first U.S. constitution.

9th9370

Students love us — and so will you.

4.6/5App Store

4.7/5Google Play

The app is very easy to use and well designed. I have found everything I was looking for so far and have been able to learn a lot from the presentations! I will definitely use the app for a class assignment! And of course it also helps a lot as an inspiration.

Stefan SiOS user

This app is really great. There are so many study notes and help [...]. My problem subject is French, for example, and the app has so many options for help. Thanks to this app, I have improved my French. I would recommend it to anyone.

Samantha KlichAndroid user

Wow, I am really amazed. I just tried the app because I've seen it advertised many times and was absolutely stunned. This app is THE HELP you want for school and above all, it offers so many things, such as workouts and fact sheets, which have been VERY helpful to me personally.

AnnaiOS user